Donald Trump’s “liberation day” tariffs present a severe risk to a US economy that is already rapidly losing momentum, with economists warning of surging prices for households and a growing risk of recession in the wake of the president’s announcements.

The combination of a baseline duty of 10 per cent with double-digit top-up tariffs on major partners including China and the EU would drive up prices for a vast array of imports, damage business investment and deepen the risk of a period of high inflation and weak growth, said analysts.

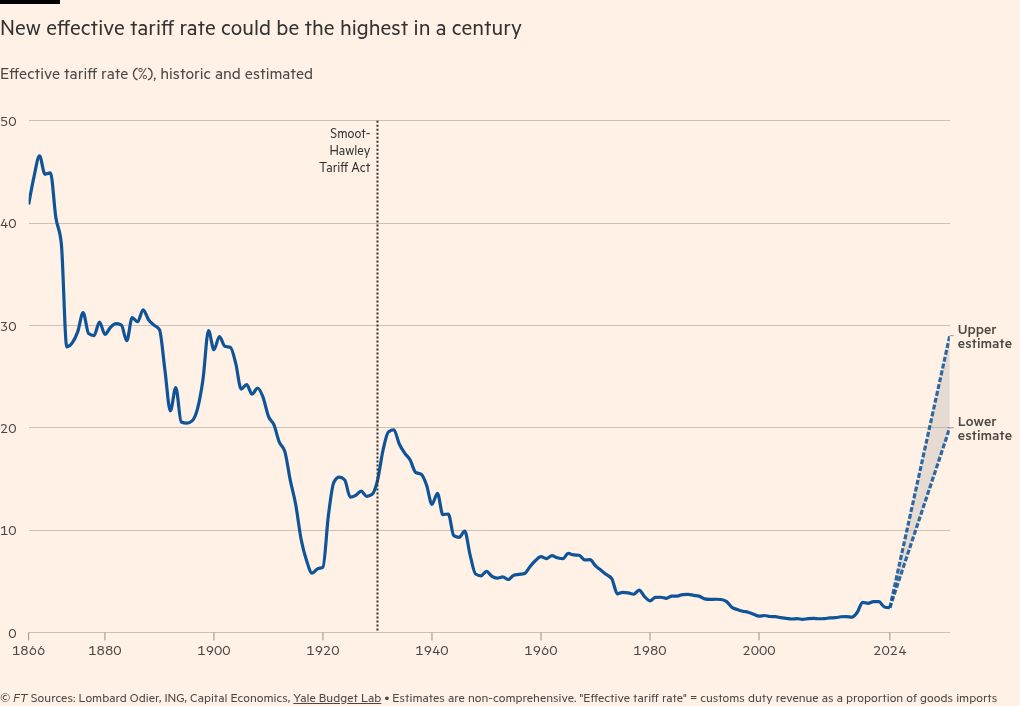

Olu Sonola, head of US economic research at Fitch Ratings, said the US tariff rate on all imports would be 22 per cent, compared with 2.5 per cent last year, putting it at the highest level since 1910. This is a “game changer” for the US economy and the world at large, he said. Analysts at Barclays forecast US output would fall in the fourth quarter of this year.

Simon French, chief economist at Panmure Liberum, said: “The chances of a US recession over the next 12 months are materially higher as a result of the decisions last night.”

Trump inherited an expanding economy with Wall Street buoyed by speculation that his deregulation and tax-cutting agenda would stoke GDP growth. Instead, expectations have taken a sharp turn for the worse as the president’s volatile approach to trade policy has led companies to defer investment decisions.

After Trump’s tariffs announcement, the dollar fell 1.7 per cent against a basket of trading partners’ currencies by early Thursday afternoon European time, reflecting rising concern about US growth prospects.

The economic impact on the US will hinge heavily on how much of the package actually goes into place, how quickly elements get dialled back as a result of negotiations with partners, and how US monetary policy responds to a combination of surging inflation and diminished growth.

Steven Blitz, economist at the consultancy TS Lombard, said the imposition of tariffs was “not a mild stagflationary event, this is a recession-producing turn — if these tariffs stay in place.”

Forecasters warned that the hit to the US economy from Trump’s new tariffs would materialise via a number of channels. While companies will not pass on 100 per cent of the extra costs to households, US consumers will fail to escape the sweeping scope of the tariffs. During Trump’s last trade war in 2018, about 60 per cent of a temporary 20 per cent US tariff on imported washing machines was passed on to consumers, analysts calculated.

James Knightley, US economist at ING, estimated that the Trump package could add $1,350 of extra costs for every American, depending on the degree of pass-through by businesses to their consumers.

Marc Giannoni, economist at Barclays, said the US president’s long-awaited reciprocal tariff announcement suggests an increase in traded-weighted tariff rates to about 23 per cent. As a result, he expected “core [consumer prices] inflation to surpass 4 per cent this year, real GDP to decline, and the unemployment rate to rise further”.

He forecast that the US economy would contract 0.1 per cent year on year in the final three months of 2025, “consistent with a recession,” and the unemployment rate would rise to rise to 4.6 per cent by the fourth quarter.

Paul Donovan, economist at UBS, said: “If there is no retreat, markets will price a US recession. If there is a retreat, markets will assume US growth will weaken.”

With inflation above the Federal Reserve’s 2 per cent target this year, the central bank faces a difficult task in keeping price growth in check at a time of rising inflation expectations. The Fed must do this while also facing calls for it to cushion slower growth caused by the worsening trade war.

Business confidence has already suffered given the volatility of Trump’s trade policies, and uncertainty will continue to drag on investment amid a period of protracted negotiations with US partners that will now ensue.

Predictions compiled in March by Consensus Economics suggested US business investment would rise by just 1.9 per cent this year, down from more than 2.5 per cent forecast until January.

The prospects of retaliation by US trading partners will damage overseas sales by American exporters, analysts said, further crimping GDP. If the sell-off in equity markets triggered by Trump’s announcements continues in the coming days, it will further weigh on sentiment.

“Tariffs will negatively affect the economy by temporarily raising import prices, reducing the Federal Reserve’s ability to cut policy rates, reducing corporate profits and investment, driving up economic uncertainty, tightening financial conditions, and forcing other countries to retaliate against American exports,” said Matt Gertken, chief geopolitical and US strategist at BCA Research.

Forecasters had already downgraded their expectations for US growth heading into Trump’s tariff announcement, with the Fed and the OECD among the institutions that trimmed GDP growth projections and warned of higher inflation.

The Atlanta Fed GDPNow tracker pointed to a 1.4 per cent annualised contraction in the first quarter, adjusted for the impact of large inflows of gold into the US.

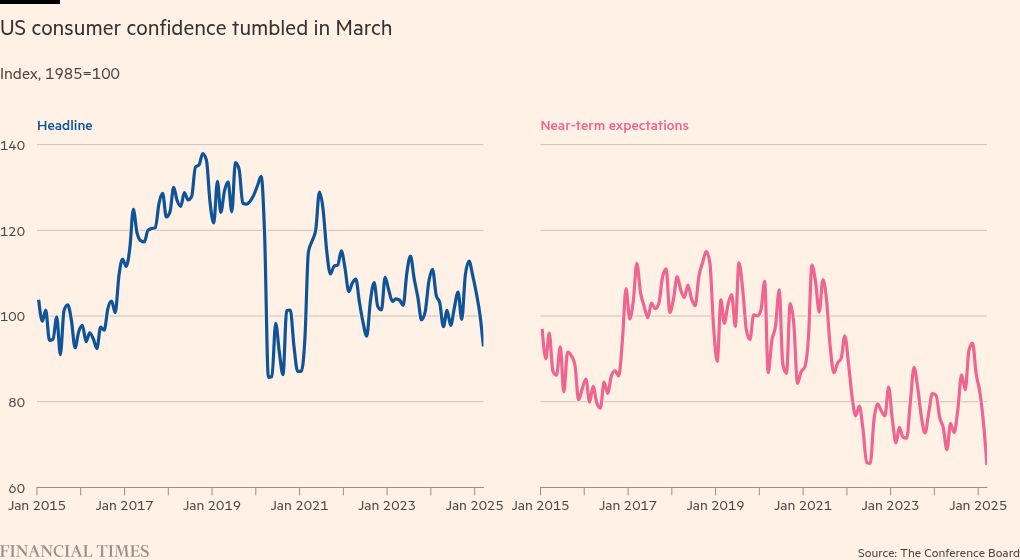

Sentiment among households has also been wilting. The Conference Board Consumer Confidence Index fell by 7.2 points to 92.9 in March, the lowest since January 2021, when some pandemic restrictions were still in place.

The consumer expectations index, based on consumers’ short-term outlook for income, business, and labour market conditions, plunged to 65.2 in March the lowest level in 12 years and well below the threshold of 80 that usually signals a recession ahead.

A question now is whether the hundreds of billions of dollars in additional tariff revenue that Trump predicted would be raised would be used to curb the deficit or injected into the economy in the form of tax cuts, said Neil Shearing, chief economist at Capital Economics.

If it is used to pay down the budget deficit then the US economy “would be lucky to avoid a recession,” he said. “If it is given back to consumers via other tax cuts, then economic growth may not suffer too badly.”

But the impact of tariffs on US growth will also depend heavily on the extent to which Trump delays or dials back the “reciprocal” element of the tariffs as traditional partners such as the EU seek to easy the severity of the measures via negotiation.

While the 10 per cent baseline tariff will apply to imports from all countries excluding Canada and Mexico with effect from April 5, the additional tariff, calculated by reference to bilateral trade deficits, will come into force later, on April 9. The fact that they were structured separately implies there is room for negotiation on the latter component, economists said.

The US now faced “near-term fears of falling output, rising unemployment, elevated inflation and stressed financial markets”, said Knightley at ING. “The key question is will Donald Trump reverse course if the economic pain becomes too much?”

{kind=link}